The economic foundation of the software industry is currently undergoing a violent reconfiguration as the era of zero-marginal costs evaporates under the immense weight of artificial intelligence. For nearly three decades, the Software-as-a-Service model thrived on the financial miracle that once the initial code was written, the cost of delivering that software to an additional million users was essentially nonexistent. This logic allowed companies to scale with astronomical gross margins, often exceeding eighty percent, because a digital copy of a program does not require raw materials or physical labor to replicate. However, the integration of generative models has fundamentally broken this physics, introducing significant and variable expenses for every single user interaction, query, and generation. We are witnessing the arrival of a material reality in a field that was once purely intangible, forcing a reckoning for every provider who built their growth projections on the assumption that scale always leads to increased profitability.

The Transformation: From Zero-Marginal Cost To Material Reality

Historically, the beauty of software lay in its incredible scalability and near-perfect margins which allowed small teams to build global empires with minimal overhead once the product reached market fit. A company could develop a sophisticated enterprise tool and see profit margins skyrocket as its user base expanded because the technical cost of serving the millionth customer was identical to the cost of serving the first. This “digital alchemy” made software the most lucrative business model in history, attracting trillions in venture capital and public investment. Artificial intelligence has decisively ended this miracle by making every query a metered event that consumes real-world resources like electricity, specialized cooling, and expensive GPU time. This shift represents what analysts now call the second death of the SaaS industry, where the underlying economic structure is no longer compatible with the traditional recurring revenue models that defined the previous era of computing.

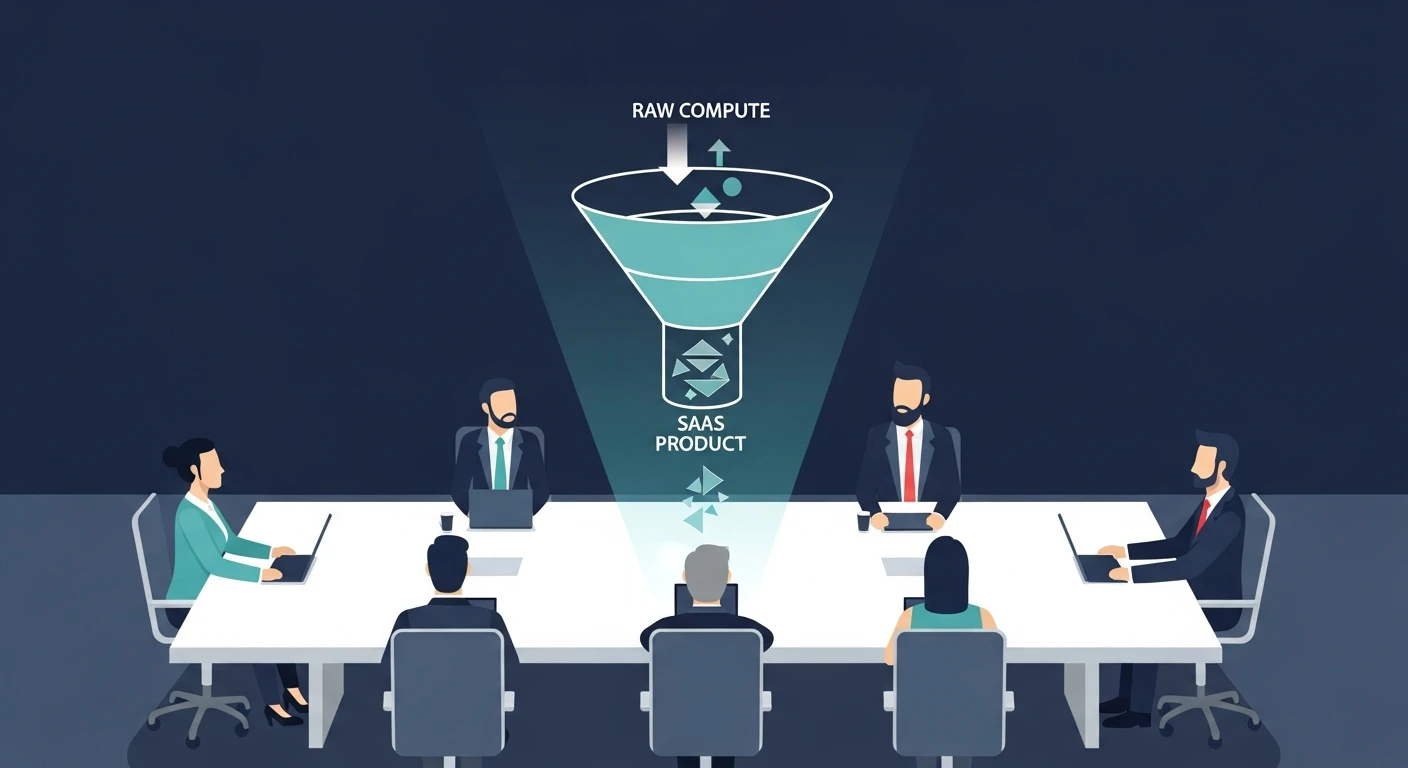

Modern software now possesses a relentless metabolism, where the execution of sophisticated code requires a constant and expensive feeding of hardware resources and token generation cycles. This dramatic change has forced developers to consider a bill of materials for their products, a concept that was previously reserved for physical manufacturing or heavy industry but is now applied to the intangible world of code. When a user asks an AI agent to summarize a legal document or generate a marketing strategy, that action triggers a chain of events across a massive supply chain of hardware that costs cents or even dollars to complete. This variable expense creates a persistent ceiling on profitability that traditional software firms never had to face, leading to a permanent change in how software is valued by both builders and buyers. Software is no longer a static tool that sits on a server; it has become a consumable commodity that disappears as it is used, much like fuel or electricity.

The Power Dynamic: Upstream Producers And Downstream Refiners

To understand the current crisis, one can look at the relationship between upstream producers and downstream refiners in the global oil and gas industry as a relevant historical parallel. Silicon manufacturers and the primary foundation model laboratories now act as the upstream giants, controlling the “crude intelligence” and the massive hardware clusters required to refine that intelligence into usable data. These entities hold the true power in the new technology supply chain because they own the scarce resources that everyone else needs to function. They set the prices for API access and compute time, leaving the application-layer companies to scramble for leftovers. This hierarchical shift has turned many famous software brands into mere intermediaries who have very little control over their own cost structures, making them vulnerable to price spikes and availability issues that they cannot mitigate through traditional software engineering.

Software companies have effectively been relegated to the role of refiners who must purchase expensive feedstock from sources they do not control and can barely influence. They process this raw compute into a finished user interface and attempt to sell it to a market that has become accustomed to stable, predictable pricing for over twenty years. This positioning makes them the primary casualties of any volatility in the hardware market or any change in the licensing terms of the foundational models they rely upon. If the cost of a token increases by ten percent, a traditional SaaS provider may see their entire profit margin for that user disappear instantly. This leaves software firms vulnerable to what traders call the “crack spread,” where the difference between the price of raw compute and the price of the finished service is constantly narrowing, forcing them to adopt defensive habits like hedging compute contracts or including aggressive pass-through clauses in their enterprise agreements.

The Financial Erosion: Why Flat-Fee Subscriptions Are Failing

The all-you-can-eat buffet model that characterized the peak years of the subscription economy is quickly becoming a massive financial liability for software providers. This model was only sustainable when the marginal cost of usage was negligible, allowing the heavy users to be balanced out by the casual users who barely touched the software. However, artificial intelligence has turned every user interaction into a tangible expense that the vendor must cover out of their own pocket, making the promise of unlimited access a dangerous financial gamble. If an enterprise customer decides to automate their entire workflow using an AI-integrated tool, they could theoretically trigger millions of dollars in compute costs while only paying a fixed monthly fee of fifty dollars per seat. This mismatch between revenue and cost is causing a quiet panic among chief financial officers who are watching their unit economics crumble under the weight of generative features.

Venture capital formerly subsidized the high cost of early AI features to gain market share and project growth, but these subsidies are rapidly disappearing as investors demand better unit economics and real paths to profitability. As a result, software is evolving from a static service into a vendor of raw machine cognition where every action must be scrutinized for its financial impact on the bottom line. The traditional seat-based model is failing because a single user can now trigger thousands of dollars in compute costs in a single afternoon if they are utilizing advanced agents. We are seeing the rise of ruthless efficiency maneuvers as companies realize they can no longer afford to host unprofitable users who consume more in compute than they pay in subscription fees. Much like surge pricing in transportation or data caps in telecommunications, software vendors are looking for ways to link their revenue directly to the fluctuating costs of their backend operations.

The New Logic: Tokens Credits And Commercial Primitives

The industry is rapidly adopting a grammar of the meter, moving toward technical billing units like the token which serves as the fundamental measurement of AI effort. This metric functions very much like a kilowatt-hour on a municipal power grid, measuring the discrete fragments of machine thought and text generation used by a customer during a session. However, because tokens are difficult for human beings to predict or visualize, they are often hidden behind more user-friendly abstractions that attempt to soften the blow of metered billing. Companies are trying to find a middle ground between the transparency of usage-based pricing and the predictability that corporate procurement departments demand. This tension is leading to a fragmented landscape where different vendors use different metaphors for cost, making it increasingly difficult for customers to compare the true value of competing software solutions.

To avoid confusing or scaring away users who are used to the simplicity of subscriptions, many firms use credits as a form of private currency to mask necessary cost increases. These credits allow companies to adjust the price of specific tasks internally without changing the advertised sticker price, providing a buffer against the volatility of the underlying compute market. It creates a walled kingdom where the vendor controls the value of the internal currency, often resulting in silent price hikes where a specific task that once cost ten credits suddenly costs fifteen. This obfuscation is a tactical necessity for companies trying to survive the transition, but it risks damaging the trust that has been built over decades between software vendors and their clients. Some vendors are even experimenting with outcome-based pricing, where they only charge for completed actions or resolutions, but this turns software into a labor-like service with significant performance risks.

Case Studies: Market Turbulence And Pricing Instability

The volatility of this transition is clearly evident in the sheer volume of pricing changes and plan restructurings occurring among the world’s major software firms. In the last twelve months alone, market trackers have observed thousands of packaging shifts as organizations try to figure out what their products are actually worth in this high-cost environment. This indicates an industry trying to discover its identity in real-time while being buffeted by the winds of technological change and hardware scarcity. Large enterprises that once signed five-year fixed-price contracts are now finding themselves back at the negotiating table as vendors realize those old contracts are no longer viable. This constant state of flux has created a sense of exhaustion among procurement teams who can no longer rely on the budget stability that used to be a hallmark of the digital era.

Major players like GitHub and Replit have experienced significant backlash from their core communities after shifting toward metered or effort-based pricing models that felt restrictive to long-time users. These rapid pivots often result in developer revolts when users find their monthly allowances exhausted in a fraction of the time they expected, leading to a loss of goodwill and a search for cheaper alternatives. Even industry leaders like Salesforce are struggling to settle on a consistent value for autonomous agents, moving through several different pricing iterations in a very short period. This instability proves that even the most established companies do not have a clear answer to the problem of AI costs. The market is currently a laboratory of failed experiments, where every new pricing tier is a guess at how much value an AI can provide versus how much it costs to run the inference.

Geopolitical Arbitrage: The Strategic Turn Toward Efficiency

In a desperate bid to protect their margins from the high cost of American-made hardware and foundational models, many software firms are quietly turning toward low-cost alternatives developed abroad. This strategic shift involves using thrifty, high-efficiency models from firms like DeepSeek to handle mundane tasks that do not require the expensive, frontier-level intelligence provided by domestic giants. Efficiency is rapidly becoming more important than raw power for companies that need to serve millions of customers without going bankrupt. By offloading simpler tasks to cheaper models, these companies can maintain their functionality while significantly reducing their “cost of goods sold.” This is a form of geopolitical arbitrage designed to defend the bottom line in an era where the cost of being “cutting edge” has become prohibitively expensive for most application developers.

Companies are increasingly acting as routing layers, choosing the cheapest adequate engine for a specific task to keep their products affordable for the mass market. This strategy allows them to maintain a facade of high-end capability while actually optimizing for the lowest possible cost behind the scenes through complex orchestration. If a user asks a simple question, it gets routed to a cheap model; if the user asks a complex question, only then is the expensive frontier model engaged. This tiered approach to intelligence is the only way many companies can survive, yet it requires a level of engineering sophistication that many traditional SaaS firms simply do not possess. It turns the role of the software developer into that of a cost-manager, where every architectural decision is viewed through the lens of compute efficiency rather than just feature sets or user experience.

The Future Landscape: Structural Realignment And Margin Compression

The financial profile of the entire software sector is changing as gross margins drop from the traditional eighty percent range toward something closer to fifty or sixty percent. This shift transforms software from a high-margin growth engine into something that looks more like a traditional infrastructure or utility business. Investors are becoming more skeptical and demanding higher returns elsewhere as they realize they now own assets with heavy variable costs and unpredictable scaling laws. The “SaaS premium” that once dominated Wall Street is fading as the reality of high-cost inference sets in, leading to lower valuations and a more conservative approach to product development. This is not just a temporary dip but a fundamental resetting of expectations for what a software company can and should be in the age of intelligence.

This transition is also creating a new form of “token inequality” within organizations, where access to superior AI models becomes a source of internal hierarchy and friction. Compute is becoming a strictly managed resource rather than a default utility, and office politics now frequently revolve around who holds the keys to the most powerful models for their specific projects. This changes the social and operational fabric of the modern workplace, as managers must now justify every “intelligent” action based on a strict cost-benefit analysis. Ultimately, the application layer is being reinvented as a bargaining layer that brokers access to the cheapest available intelligence for its users. The era of predictable, high-margin software is over, and the industry must now adapt to a world where code is subject to the same inflationary pressures and material constraints as any other industrial process.

Strategic Imperatives: Adapting To The Era Of High-Cost Compute

The industry recognized that survival depended on a complete departure from the legacy structures of the previous decade. Successful organizations quickly pivoted away from universal seat-based pricing and implemented sophisticated, multi-tiered consumption models that aligned their revenue directly with the underlying compute costs. They stopped treating AI as a free feature to be added to every menu and started treating it as a premium resource that required its own distinct economic logic. By building robust internal systems to track token usage at the granular level, these companies regained control over their margins and provided their customers with the transparency needed to justify higher expenditures. This shift required a difficult conversation with stakeholders about the end of the “unlimited” era, but it was the only path toward long-term sustainability in a market defined by silicon scarcity.

Developers and architects focused their energy on model distillation and the deployment of small, specialized language models that could run locally or on cheaper infrastructure. They moved away from the “bigger is better” mentality and embraced a philosophy of “just enough intelligence” for the task at hand. This approach reduced the reliance on expensive third-party APIs and allowed firms to reclaim their autonomy from the giant model labs. Furthermore, the most resilient players established “compute budgets” for their users, treating digital intelligence like a finite corporate asset rather than an infinite tap. These steps ensured that software remained a viable business, even as the raw materials of the industry became more expensive. The industry ultimately learned that while the cost of machine thought was high, the cost of failing to account for it was significantly higher.